America’s Biggest Bank Is Everywhere—and It Isn’t Done Growing

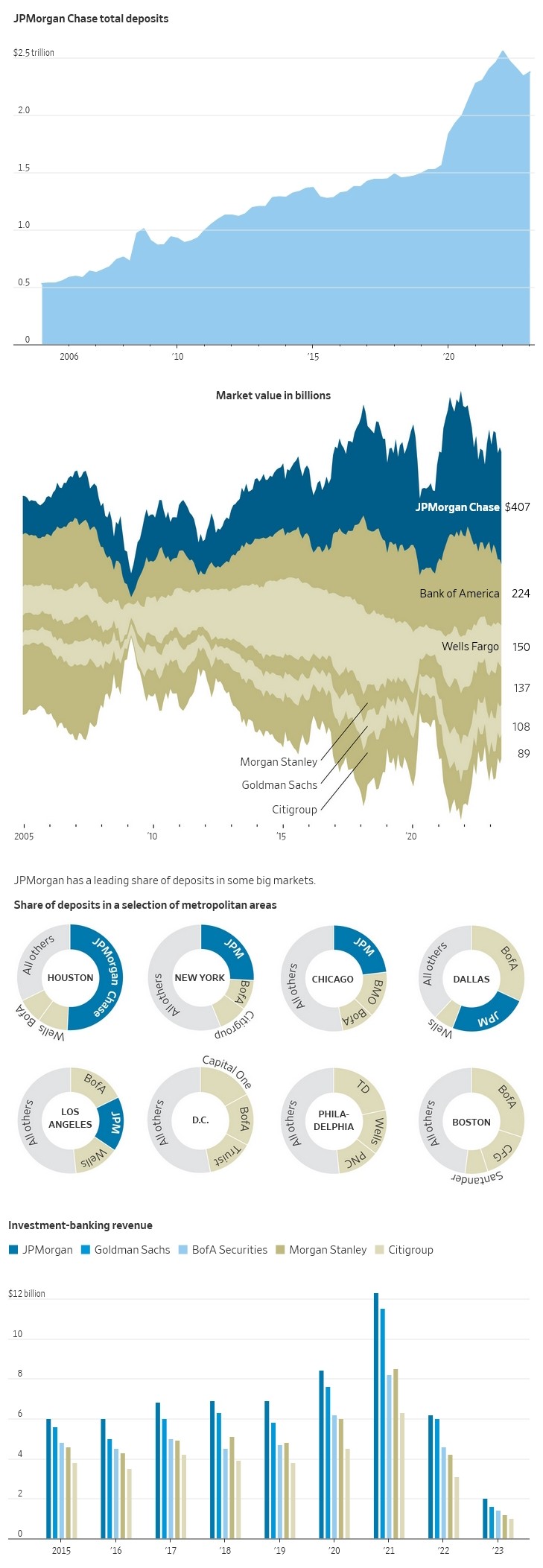

Thousands of banks call the U.S. home. Among them, JPMorgan Chase stands alone. The bank has opened branches in 25 new states, plus Washington, D.C., since 2018. Its nearly 4,800 locations are in every state in the Lower 48, an achievement it alone has unlocked. It added another 93 earlier this month when it bought First Republic Bank in a government-backed fire sale. It now has more than 13% of the nation’s deposits and 21% of all credit-card spending, a bigger share in each than any other bank. Its investment bankers bring in more revenue than all of their Wall Street rivals, including Goldman Sachs and Morgan Stanley.

America’s biggest bank is also a travel agency for big spenders and a media company serving up restaurant recommendations. Its Morgan Health unit is trying to transform employer-sponsored healthcare. The Institute, its D.C. think tank, advises government decision makers using the bank’s reams of customer spending, saving and borrowing data. When the banking system faced a crisis of confidence this spring, JPMorgan’s heft was a ballast. Customers sent it $50 billion in new deposits. Employees at stricken banks sent résumés. Treasury Secretary Janet Yellen called CEO Jamie Dimon for help.

Yet JPMorgan’s show of strength, for many, exposed a weakness in the U.S. financial system. The bank and its largest rivals have become so big, their reach so extensive, that the government would almost surely step in to prevent their failure. That implicit guarantee encourages people and businesses to move their money to them in times of stress creating a feedback loop that makes big banks bigger at the expense of their smaller peers.

Smaller banks support industries and regions that megabanks aren’t especially good at serving, said Gene Ludwig, the former head of the Office of the Comptroller of the Currency, one of the banking system’s top regulators. “We have a premier bank that’s shown itself to be well run,” said Ludwig, who now heads a financial-services advisory firm. “But we need a diverse banking system.”

JPMorgan isn’t done getting bigger. At its annual investor day Monday, Dimon and his lieutenants will be quick to play down the bank’s dominance, detailing plans to grow in the markets and products where it isn’t already No. 1. Chief among them is managing its customers’ wealth, one of First Republic’s premier offerings. “The message from investor day is: ‘We are JPMorgan, hear us roar,’” said Mike Mayo, a bank analyst at Wells Fargo. JPMorgan has a leading share of deposits in some big markets. In markets where the bank had a lower share of in deposits, it has expanded in recent years.

In March, the deposit run that claimed Silicon Valley Bank and Signature Bank in a matter of days was spreading throughout America’s regional banks. First Republic lost $100 billion in deposits in a matter of days. Dimon, at Yellen’s prodding, rallied his fellow big-bank CEOs to deposit $30 billion into First Republic to shore up confidence in the troubled lender. Behind the scenes, JPMorgan executives began studying the possibility of buying First Republic should rescue efforts fail. The San Francisco-based bank had a slew of rich customers and a ready-made wealth-management business, something JPMorgan was painstakingly building on its own.

First Republic’s loyal following among the West Coast elite would give JPMorgan’s bankers access to another group it long coveted: tech entrepreneurs with lots of money to manage and companies to someday take public. Those customers could become a valuable source of business for its investment bank, which tends to balance out the consumer operation in a downturn. JPMorgan bankers have outearned all their rivals advising on stock and debt sales and mergers every year for the last decade, according to Dealogic.

Dimon and his deputies had been in this position before. JPMorgan’s 2008 purchase of the failed Washington Mutual helped kick off the bank’s nationwide expansion. In the years after the financial crisis, JPMorgan focused on growing its relationship with the nation’s wealthy. It built its credit-card operations into a giant, launching its Ultimate Rewards and Sapphire brands. The goal was to forge relationships that, with each new credit card, mortgage and brokerage account, become harder to break.

Courting America’s mass affluent had become something of an obsession at JPMorgan. Executives hunted for deals that would give them an in with the upwardly mobile. Their efforts didn’t always pan out. In 2021, JPMorgan paid $175 million for Frank, a little-known startup that helped would-be college students apply for financial aid. A year later, it sued the founder, Charlie Javice, accusing her of fabricating most of its users. Javice was indicted on fraud charges and has denied wrongdoing. “A huge mistake” is how Dimon has described the saga.

Dimon was determined to get it right with First Republic. Hundreds of JPMorgan employees studied First Republic’s balance sheet. They zoomed in on maps of First Republic’s branch network and vetted the real-estate value, neighboring shops and foot traffic, putting to use research tactics they used when JPMorgan was on its branch-building march across the country. Top executives divided up first-day assignments should a deal come together. Marianne Lake and Jennifer Piepszak, the co-heads of JPMorgan’s consumer bank, would make the trip to First Republic’s San Francisco headquarters and manage the integration. It was a high-stakes assignment for the two women, who sit atop the list of candidates to eventually succeed Dimon as CEO.

On the last Friday in April, the Federal Deposit Insurance Corp. decided First Republic was out of time. The JPMorgan machine kicked into high gear. A team of nearly 1,000 pored over First Republic’s financial information. On Saturday, Dimon and his top lieutenant, Daniel Pinto, chaired an all-day gathering of top executives that included a series of presentations about what First Republic could do for the bank’s various businesses. “It felt like a finely tuned orchestra,” Piepszak said in an interview. “We knew what we knew and what we didn’t know.”

First Republic’s wealth-management arm was of particular interest. In 2019, JPMorgan announced it was launching a new business to cater to wealthy people who had fallen between the cracks of its retail branches and private bank for the ultrarich. The idea was to capture some of the $4 trillion in assets that JPMorgan depositors were keeping at other wealth managers like Morgan Stanley and Bank of America. Four years later, JPMorgan still lagged well behind its rivals. It has a goal to get to $1 trillion in assets under management. First Republic would put it within spitting distance.

PNC Financial, Citizens Financial and Fifth Third Bank also made a run at First Republic in the FDIC-led auction. But the deal was JPMorgan’s to lose. With $3.7 trillion in assets, it is more than triple the size of those three combined. The deal was announced before the sun rose on Monday, May 1. Within hours, Lake and Piepszak were on a plane to California.

The deal revived a debate about the growing power of America’s biggest banks. What are the implications for the banking sector from JPMorgan’s size? Join the conversation below.

“The failure of First Republic Bank shows how deregulation has made the too big to fail problem even worse,” Massachusetts Democratic Sen. Elizabeth Warren tweeted a few hours after the deal was announced. “A poorly supervised bank was snapped up by an even bigger bank—ultimately taxpayers will be on the hook. Congress needs to make major reforms to fix a broken banking system.”

Dimon, for his part, said JPMorgan’s ability to swallow up most of First Republic’s deposits and loans shows that the system is working as it should. “We need large, successful banks in the largest and most successful economy in the world,” Dimon said on a call with reporters to discuss the deal. “And anyone who thinks that it’d be good for the United States of America not to have that, you call me directly.”

JPMorgan executives have been on the road in the weeks since, visiting First Republic branches and meeting stunned employees, some of whom will lose their jobs. JPMorgan is considering remaking the First Republic locations into special branches for affluent customers, luxurious spaces where they could seek investing and estate-management advice. Success hinges on the bank’s ability to convince First Republic’s financial advisers to stay, despite the banks’ different compensation structures.

Lake and Piepszak are treading lightly, preserving the First Republic high-touch, small-bank model while integrating it into their gargantuan bank. “We want to not break it,” Lake said. “We have to do it in a way that works for this company.”