At last count, there were 172 venture-backed startups valued at $ 1 billion or more. That’s an unprecedented number. And while private valuations are not indicative of market cap, at least a dozen of those unicorns would have a shot at making the S&P 500 if they went public, in my estimation.

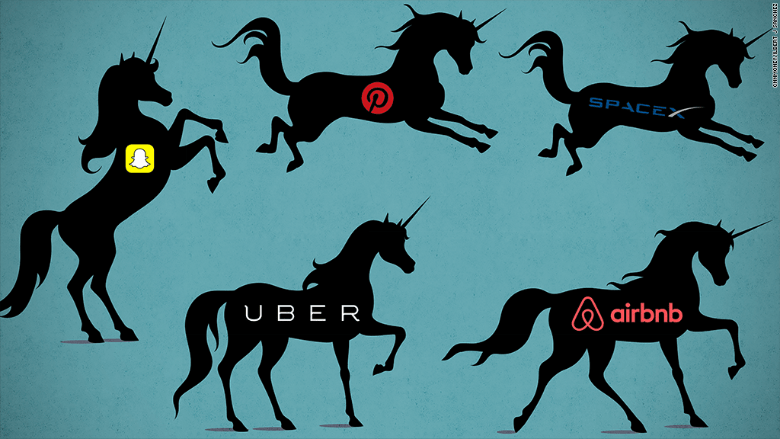

Now guess how many unicorn IPOs we’ve seen so far this year. If you said zip, you were close. There was Twilio and, well, that was it. And there were all of four in 2015, including Box, Pure Storage and Square. That’s just pathetic. Where are the big beasts? Where is Uber? Airbnb? Palantir? Snapchat? Pinterest?

The real question is, what gives? Why the unprecedented number of late-stage, high-value startups stuck in a perpetual pre-IPO pipeline? And more important, is that likely to change anytime soon?

The answers actually have little to do with public markets and everything to do with venture capital. When private investors start getting burned and stop throwing enormous amounts of capital at startups like they’re sure bets, that’s when we’ll see unicorns stampede on Wall Street.

It’s been two years since Benchmark partner Bill Gurley first sounded the alarm that the private equity market was out of control. One of Silicon Valley’s most successful venture capitalists and author of the popular Above the Crowd blog, Gurley cautioned that investors were taking on too much risk, funding high burn-rate startups with no profits at sky-high valuations.

That warning led to many others, including venture capitalist Marc Andreessen’s infamous swimming trunks tweet:

It took a while for folks to get comfortable with the dreaded “B” word, but before long, everyone from Snapchat CEO Evan Spiegel to AOL founder Steve Case to Mark Cuban were talking tech bubble. Case and Cuban should know. They both made a bundle off the dot-com bubble, the former in the ill-fated AOL-Time Warner merger and the latter selling broadcast.com to Yahoo for $ 5.7 billion. Both deals went bust.

It’s a bit different this time around, but it’s still inevitable: what goes up, must come down. After 12 consecutive quarters of growth, global venture funding fell off a cliff in the fourth quarter of 2015, and has remained essentially flat since. Meanwhile, the total number of deals has now declined for four straight quarters, according to CB Insights, which tracks that sort of thing.

In another sign that the gravy train is over, down events, where valuations decline relative to previous rounds, ballooned to 57 over the past nine months, compared with just 22 during the first three quarters of 2015. Some notable unicorns that took big haircuts included Zenefits, Xiaomi, Flipkart, Jawbone and Foursquare.

Make no mistake, down rounds are painful events, both emotionally and financially. They can dampen momentum and hurt morale, not to mention the obvious increase in the cost of capital relative to equity.

Everyone around these parts knows that the pain is far from over. Ironically, that’s a good thing.

The bubble hasn’t exactly burst, but it’s deflating enough to bring sense and sensibility back to the startup world. Whereas the previous mantra was growth at all cost, founders are tightening their belts and cutting their burn rates in an effort to deliver quality growth with a renewed emphasis on profitability.

Meanwhile, every bubble has its own unique characteristics. This one has been defined by $ 100 million plus private mega-round deals that have taken the place of IPOs. There were 35 such rounds last quarter. While still a big number, it represents a five-quarter low and a steep decline from 63 mega-rounds during the same quarter of 2015.

Now let’s put all that in context.

Venture capital firms can’t go on ad infinitum without some big exits – IPOs and acquisitions that return profits to the limited partners who invest in their $ 1 billion funds. And let’s face it, these unicorns aren’t getting any younger. Airbnb has been around for eight years. Spotify is 10. Palantir is 12. Jawbone is nearly 17 years old.

If venture capitalists can maintain their newfound discipline and effectively manage risk, they will remain in control of what has finally returned to a buyer’s market. And with Wall Street indexes trading near record highs, that can only mean one thing: When the time is right, high-quality unicorns will once again raise capital in the public markets.

Steve Tobak is a management consultant, columnist and author of “Real Leaders Don’t Follow: Being Extraordinary in the Age of the Entrepreneur.” He runs Silicon Valley-based Invisor Consulting and blogs at stevetobak.com.