Warren Buffett’s Top 10 Dividend Stocks With The Highest Yields

Warren Buffett (Trades, Portfolio) is arguably the greatest investor of all time. He has grown his wealth by investing in and acquiring business with strong competitive advantages trading at fair or better prices. This investment style has served Warren Buffett (Trades, Portfolio) well – his net worth is now over $ 70 billion.

A total of 89.5% of Warren Buffett (Trades, Portfolio)’s portfolio is invested in dividend stocks. Many of these dividend stocks have paid rising dividends over decades. Warren Buffett (Trades, Portfolio) prefers to invest in shareholder friendly businesses with long track records of success. It happens that dividend stocks with long histories of dividend increases match what Warren Buffett (Trades, Portfolio) looks for in a stock investment.

Warren Buffett (Trades, Portfolio)’s Portfolio

Warren Buffett (Trades, Portfolio)’s portfolio currently consists of 47 stocks. Of these, 33 are dividend stocks. Warren Buffett (Trades, Portfolio)’s portfolio as a whole generates a dividend yield of 2.17%; about 15% higher than the S&P 500’s dividend yield.

Warren Buffett (Trades, Portfolio)’s top 6 holdings make up over 70% of his portfolio. These 6 stocks represent Warren Buffett (Trades, Portfolio)’s highest conviction picks based on the amount of money he has invested in them. All of his top 6 holdings are dividend stocks. His top 6 holdings have a portfolio weighted dividend yield of 2.53%, well above the average of his portfolio. Three of the top 6 are Dividend Aristocrats.

You can download Warren Buffett (Trades, Portfolio)’s full portfolio of 47 stocks by clicking the button just below this paragraph. The spreadsheet includes dividend yield and the percentage each stock holding is of Warren Buffett (Trades, Portfolio)’s total portfolio.

Warren Buffett (Trades, Portfolio)’s Top 20 Highest Yielding Dividend Stocks

Each of Warren Buffett (Trades, Portfolio)’s top 20 highest yielding dividend stocks are analyzed below. Relevant metrics including price-to-earnings ratio, dividend history, current dividend yield, and historical growth rate are shown to give an idea of the relative investment merit of each business. Reviewing Warren Buffett (Trades, Portfolio)’s highest yielding dividend stocks may give you new ideas on how to improve your portfolio.

10 – Deere & Company (DE)

Dividend Yield: 2.72%

Price-to-Earnings Ratio: 11.52

Years of Steady or Rising Dividends:

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 1.41%

10 Year Earnings-Per-Share Growth Rate: 12.7%

Deere & Company is the largest manufacturer of farming machinery in the world. Deere & Company also manufactures forestry and construction equipment. In addition, the company operates a financing division to help customers finance expensive equipment.

Deere & Company is one of Warren Buffett (Trades, Portfolio)’s most recent purchases. The company is a timely buy as it is nearing its cyclical trough which historically reduces the company’s earnings and share price. This gives long-term investors a chance to pick up shares of this high quality business for a discount. With a price-to-earnings ratio of just 11.5, Deere & Company appears to be significantly undervalued. Peak earnings during the company’s last cyclical peak were $ 9.08 per share. During the next peak, the company should see earnings-per-share of at least $ 10 per share. The company has traditionally had a price-to-earnings ratio of around 10 during peak earnings years which will result in a share price of at least $ 100 when the company reaches its cyclical peak. At current price, Deere & Company is likely undervalued by at least 10%.

The company’s competitive advantage comes from its brand recognition and reputation for quality in the farming machinery industry. Deere & Company’s competitive advantage has given it a 60% market share of the farming equipment industry in the US and Canada.

Long term growth prospects are bright for Deere & Company. Increased affluence and population growth in emerging markets will likely drive demand for food, grains, and farming equipment globally. Over the last decade, Deere & Company has averaged EPS growth of over 12% a year. The company should continue to grow EPS at a double-digit rate over full market cycles going forward. This will result in more-than-satisfactory returns for shareholders. In addition to solid growth, Deere & Company currently has a dividend yield of around 2.7%, which provides current income for dividend stock investors.

9 – Johnson & Johnson (JNJ)

Dividend Yield: 2.80%

Price-to-Earnings Ratio: 17.97

Years of Steady or Rising Dividends: 53

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.03%

10 Year Earnings-Per-Share Growth Rate: 6.1%

Johnson & Johnson is the world’s leading diversified health care company based on its $ 279 billion market cap. The company has grown earnings-per-share each year for 31 consecutive years – which is absolutely amazing. In addition, the company has paid increasing dividends for 53 consecutive years. Johnson & Johnson is one of the most safe and stable stocks in which to invest for long-term dividend growth.

A company cannot grow earnings-per-share for over 3 decades without a strong and lasting competitive advantage. The company has a portfolio of strong consumer brands including: Aveeno, Neutrogena, Band-Aid, Bengay, Neosporin, Listerine, Tylenol, Motrin, Benadryl, Mylanta, Zyrtec, Nicorette, Pepcid, Splenda, and Visine, among others. In total, the company’s consumer products generate about 20% of total revenues for the company.

Johnson & Johnson’s biggest profitability driver is its pharmaceutical divisions, which is responsible for over 40% of company revenue. Johnson & Johnson has a strong competitive advantage in this segment as well. The company’s research and development department and intellectual property portfolio help the company to keep its drug pipeline full. Johnson & Johnson’s massive size and strong cash flows give it a large research and development budget that smaller companies cannot match.

The company’s third segment is Medical Devices and Diagnostics. The segment is slightly smaller than the company’s pharmaceutical segment. The Medical Devices and Diagnostics segment develops, manufactures, and sells medical devices for the following medical fields: cardiovascular, diabetes, diagnostics, orthopedics, surgery, and vision.

Johnson & Johnson is currently trading for a price-to-earnings ratio of just under 18. The company is slightly cheaper than the S&P 500 despite being of a much higher quality than the average business. Johnson & Johnson will not deliver rapid growth for shareholders – earnings-per-share have grown at just over 6% a year over the last decade. With that said, the company does have a solid dividend yield of 2.8% and scores very high marks for safety.

8 – United Parcel Service (UPS)

Dividend Yield: 2.99%

Price-to-Earnings Ratio: 20.68

Years of Steady or Rising Dividends: 32

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.01%

10 Year Earnings-Per-Share Growth Rate: 3.6%

United Parcel Service is the largest publicly traded freight and delivery company in the world based on its $ 88.6 billion market cap. The company was founded in Seattle in 1907 and has grown to become a global business with close to 2,000 operating facilities and nearly 100,000 vehicles in its fleet.

The larger a delivery network gets, the stronger its competitive advantage becomes as it can ship anywhere in the world – often for less thanks to scale advantages. As the largest freight company in the world, United Parcel Service has a strong competitive advantage that will likely get strong as time goes by. The mail industry in the U.S. is an oligopoly largely dominated by just 3 players: Fed Ex, United Parcel Service, and the U.S. Post Office. Of the three, only the two publicly traded companies are profitable.

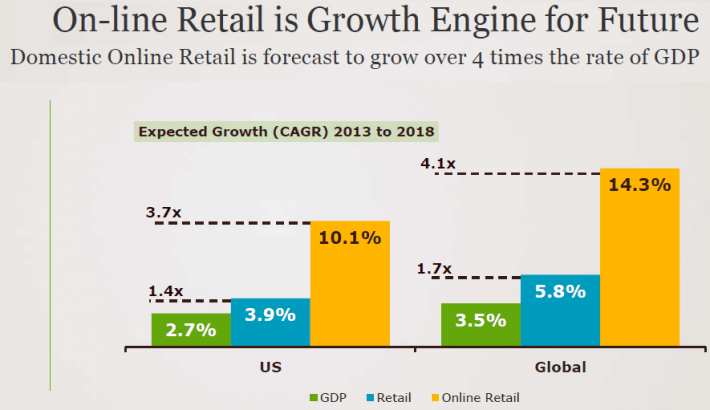

Online retail will continue to drive growth for United Parcel Service going forward as the company benefits from increased package shipments. Online retail is expected to grow about 4x as fast as global GDP over the next several years. The image below from UPS’ latest investor presentation shows this growth:

[ Enlarge Image ]

In addition to tailwinds from e-commerce growth, United Parcel Service is also benefitting from growth in emerging markets. The company has focused on expanding its international reach over the last 20 years. As global commerce grows, United Parcel Service stands to gain from increased shipments between countries. In total, the company is expecting 6% to 12% EPS growth for fiscal 2015.

United Parcel Service is a low-risk business in a fairly slow-changing industry. The company’s price-to-earnings ratio reflects the company’s strong competitive advantage and solid growth prospects. In addition, United Parcel Service is a shareholder friendly business. The company has several decades of rising dividends, and has reduced its share count by an average of 2% a year over the last decade.

7 – Procter & Gamble (PG)

Dividend Yield: 3.14%

Price-to-Earnings Ratio: 23.81

Years of Steady or Rising Dividends: 59

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 4.05%

10 Year Earnings-Per-Share Growth Rate: 5.8%

At the time of this writing, Warren Buffett (Trades, Portfolio) had agreed to exchange his $ 4.32 billion worth of Procter & Gamble shares for Duracell. Procter & Gamble is going through a transition. The company is shedding its non-core and underperforming brands to streamline operations and focus on the company’s core brands.

As a result of this transition, Procter & Gamble decided to part with its Duracell brand. Warren Buffett (Trades, Portfolio) agreed to facilitate the Duracell transaction. In the deal, Berkshire Hathaway will exchange its 52.79 million Procter & Gamble shares valued at $ 4.32 billion for the Duracell division. Procter & Gamble is also contributing about $ 1.8 billion in cash to Duracell before the spin-off. This deal is expected to close in the second half of fiscal 2015. The transaction values Duracell at about 7x 2014 EBITDA. For comparison, Procter & Gamble is currently trading at around 11.9x fiscal 2014 EBITDA.

The Procter & Gamble – Duracell swap works well for Berkshire Hathaway. The deal allows Warren Buffett (Trades, Portfolio) to exit his position in Procter & Gamble tax-free. The $ 1.8 billion in cash Duracell is receiving will come to Berkshire Hathaway tax-free as it is ‘part’ of Duracell.

Procter & Gamble has performed well since refocusing its operations on core brands. The company’s most recent earnings release shows constant-currency core earnings-per-share up 10% versus the same quarter a year ago. The company’s growth in earnings is being fueled by increasing operating efficiency and cost-cutting. Despite solid growth prospects and a shareholder friendly management, Procter & Gamble appears somewhat overvalued at this time with a price-to-earnings ratio near 24.

6 – Sanofi (SNY)

Dividend Yield: 3.17%

Price-to-Earnings Ratio: 25.43

Years of Steady or Rising Dividends: 21

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.19%

10 Year Earnings-Per-Share Growth Rate: 2.5%

Sanofi is a global pharmaceutical company with a market cap of $ 136.7 billion. The company is headquartered in Paris, France. In 2014, Sanofi generated 82% of revenue from pharmaceuticals, 12% from vaccines, and 6% from animal health products. The company has heavy exposure to emerging markets, with 36% of 2014 sales coming from these markets.

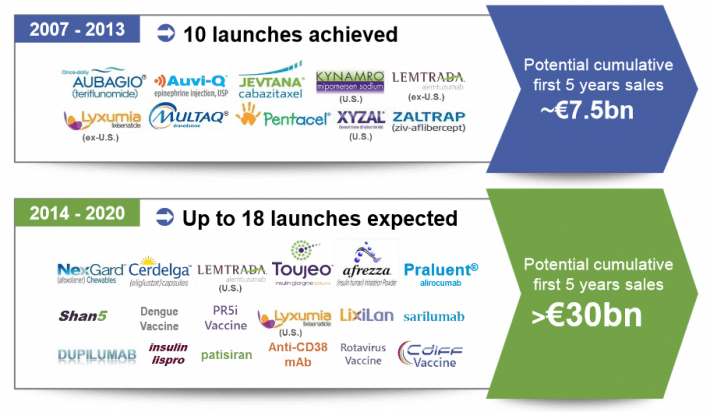

Sanofi has grown to reach a market cap well over $ 100 billion thanks to its strong research and development department. The company’s ability to roll out new and innovative treatments drives revenue. Fortunately for shareholders of Sanofi, the company’s number of product launches is increasing. From 2007 to 2013, the company launched 10 products. From 2014 to 2020, Sanofi is expecting 18 product launches. The image below from the company’s most recent presentation shows the company’s expected launches to 2020.

[ Enlarge Image ]

[ Enlarge Image ]

Sanofi is a shareholder friendly company. The company has increased its dividend payments each year for the past 21 years (measured in Euros, not USD). The company has recently begun to focus on share repurchases recently. Sanofi has reduced its net share count by about 1% in the last 2 years – with most of that coming last year. Sanofi will likely continue to increase share repurchases to increase the value of each share. Sanofi’s 3.17% dividend yield combined with its share repurchase makes for a shareholder yield of about 3.7% a year.

Sanofi’s current price-to-earnings ratio of 25.43 is somewhat higher than other high quality pharmaceutical companies. The company is expecting solid growth from its new launches over the coming several years. Nevertheless, Sanofi shares are likely somewhat overvalued at this time.

5 – Coca-Cola (KO)

Dividend Yield: 3.21%

Price-to-Earnings Ratio: 20.01 (using adjusted earnings)

Years of Steady or Rising Dividends: 53

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 15.40%

10 Year Earnings-Per-Share Growth Rate: 7.2%

Coca-Cola is Warren Buffett (Trades, Portfolio)’s second largest holding (behind Wells Fargo). Berkshire Hathaway has $ 16.44 billion invested in Coca-Cola. Coca-Cola is the global leader in ready-to-drink beverages. The company has 20 brands that generate $ 1 billion or more per year in sales, and the Coca-Cola soda brand is the most popular in the world by a wide margin.

Coca-Cola has increased its dividend payments for over 5 decades. The company clearly possesses a strong competitive advantage. Coca-Cola’s competitive advantage stems from its powerful brands. The company supports its brands by spending over $ 3 billion per year on advertising. Coca-Cola can spend more on advertising than any other beverage company (except for perhaps PepsiCo), which further reinforces its competitive advantage.

Going forward, Coca-Cola’s earnings-per-share growth will come from a mix of global expansion and operating efficiency increases. The company is using its global distribution power to leverage popular smaller drink brands and sell them worldwide. An example of this is the company’s acquisition of Monster’s non-energy drink brands like Hubert’s Lemonade and Hanson’s juice drinks. Coca-Cola is taking several steps to improve operating efficiency, including:

- Refranchise U.S. bottling operations

- Decentralize decision making

- Better align employee incentives with company goals

The company’s earnings-per-share growth plans are working. Coca-Cola’s 1stquarter resultsshowed currency-neutral operating income per share grew 13% versus the same quarter a year ago. Despite being an old company, Coca-Cola still has plenty room for growth. In addition, the company is very shareholder friendly. Coca-Cola currently has a high dividend yield of 3.2% to go with solid share repurchases. Over the last 5 years, the company has repurchased about 1.2% of shares outstanding. Share repurchases combined with the company’s dividend gives investors a shareholder yield of about 4.4%. Total returns for Coca-Cola should be over 10% going forward from dividends (3.2%) and earnings-per-share growth (7% or more per year).

4 – National Oilwell Varco (NOV)

Dividend Yield: 3.35%

Price-to-Earnings Ratio: 9.80

Years of Steady or Rising Dividends: 6

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.27%

10 Year Earnings-Per-Share Growth Rate: 23.9%

National Oilwell Varco’s stock price has fallen 23% in the last year due to the decline in oil prices. This has driven down the company’s price-to-earnings ratio, which is now just 9.80. National Oilwell Varco is the largest supplier of equipment for oil and gas drilling. The company has a market cap of $ 22 billion. National Oilwell Varco’s percentage of total fiscal 2014 revenue by segment is shown below:

- Rig Systems: 42%

- Rig Aftermarket: 14%

- Wellbore Technologies: 24%

- Completion & Product Solutions: 20%

Low oil prices will have a direct impact on National Oilwell Varco’s earnings in fiscal 2015. The company’s customers will purchase less rig and drilling systems and equipment as a result of low oil prices and resulting falling capital expenditure budgets. Fortunately, National Oilwell Varco’s management is approaching falling share prices with the right attitude. The company’s management plans to use the company’s solid balance sheet to repurchase shares at depressed prices. This will be a significant victory for long-term shareholders as share repurchases when a stock’s price is depressed generate significant value.

National Oilwell Varco currently has $ 3.146 billion in total debt and $ 4.091 billion in cash on hand. Very little of the company’s debt is due in 2015. With its current cash hoard, National Oilwell Varco has plenty of ‘dry powder’ to repurchase shares with.

Like many of Warren Buffett (Trades, Portfolio)’s other dividend stocks, National Oilwell Varco is an industry leader. The company is trading well below fair value with a price-to-earnings ratio under 10. Management is very shareholder friendly and is adept at capital allocation. The company currently sports a 3.35% dividend yield; investors get ‘paid to wait’ for the company’s price-to-earnings ratio to rise – which will likely happen when oil prices increase.

3 – General Motors (GM)

Dividend Yield: 3.35%

Price-to-Earnings Ratio: 11.64

Years of Steady or Rising Dividends: 1

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 1.37%

10 Year Earnings-Per-Share Growth Rate: N/A

General Motors famously declared chapter 11 bankruptcy in 2009. Since restructuring and going public again in 2010, the company has been profitable every year and even managed slight earnings-per-share growth averaging 1.4% a year. General Motor’s is the United States largest automobile manufacturer. The company has around 17% market share in the United States car and truck market. Around 40% of the company’s revenue is now generated overseas, in addition to its North American operations.

General Motors has strong growth prospects ahead. The company is realizing higher operating income margins now thanks to its focus on cost control. The company is seeing solid growth in its joint venture in China. China sales grew 12.1% in fiscal 2014. Growth in China should come in slower this year due to the slow-down in the company’s economy. General Motors operates in the highly competitive automobile industry. The company declared bankruptcy in 2009. Since restructuring, it has been able to keep pace with the industry, but growth has been very slow. Bottom line growth is increasing at just 1.37% a year since the restructuring, while revenue growth has 2.7%; about in line with inflation.

General Motors’ high dividend yield and low price-to-earnings ratio should appeal to value oriented investors. The company has a low payout ratio of about 40%. General Motors will likely increase dividend payments in excess of its earnings-per-share growth rate over the next several years. If General Motors were to experience better earnings-per-share growth, it would do well for investors. The company’s Chevrolet Volt EV concept – which has a 200 mile range – could potentially drive growth for the company in the future. Additionally, the company is currently restructuring operations in Russia, Thailand, and Indonesia. Cost savings from these restructurings should provide a small boost to earnings as well in the coming years.

2 – General Electric (GE)

Dividend Yield: 3.43%

Price-to-Earnings Ratio: 16.25

Years of Steady or Rising Dividends: 6

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.27%

10 Year Earnings-Per-Share Growth Rate: -1.0%

General Electric is one of the world’s largest conglomerates based on the company’s $ 270 billion market cap – although it falls about $ 80 billion short of Warren Buffett (Trades, Portfolio)’s Berkshire Hathaway.

General Electric shareholders will likely see strong returns over the next few years. The company is committed to divesting its GE Capital business and return somewhere around $ 90 billion to shareholders through dividends and share repurchases. This is about 33% of the company’s value at current prices.

General Electric spun-off its retail finance and credit card division recently, which is now named Synchrony Financial (SYF). There are rumors that General Electric will soon sell its commercial lending portfolio to Wells Fargo (Warren Buffett (Trades, Portfolio)’s largest holding) for up to $ 74 billion. If this transaction does occur, General Electric will have mountains of cash to return to shareholders.

The divestiture of GE Capital is a positive sign for General Electric shareholders. The company is focusing on what it does best – manufacturing a diverse range of products, and selling everything else to generate cash. When a management team actively seeks to make the company smaller to reward shareholders, there is a high likelihood that shareholders will see strong gains as the company regains its focus.

General Electric currently trades at a reasonable price-to-earnings ratio of 16.25. Additionally, the company has a strong 3.4% dividend yield. Investors in General Electric today will likely do much better than they have done over the last decade thanks to the company’s reasonable price-to-earnings ratio, high dividend yield, and large divestiture plans.

1 – Verizon (VZ)

Dividend Yield: 4.43%

Price-to-Earnings Ratio: 14.98

Years of Steady or Rising Dividends: 31

Percent of Warren Buffett (Trades, Portfolio)’s Portfolio: 0.70%

10 Year Earnings-Per-Share Growth Rate: 7.5%

Verizon is the highest yielding stock in Warren Buffett (Trades, Portfolio)’s portfolio with its dividend yield of 4.4%. The company is also the leader in wireless in the United States. Verizon controls 34% of the wireless market in the U.S., with AT&T (T) controlling another 31%. Verizon, AT&T, T-Mobile, and Sprint together account for 90% of the wireless industry in the United States. The oligopolistic wireless industry is not good for consumers – but great for the businesses in the industry which reap higher-than-normal profits from the lack of competition.

Verizon is focused on returning value to shareholders. The company recently announced it plans to sell its wireline assets in California, Florida, and Texas to Frontier Communications (FTR) for $ 10.54 billion. The move helps Verizon reduce its exposure to its slower growing wireline segment. Verizon also agreed to lease the rights to over 11,300 of its company owned towers to American Tower Corporation (AMT), as well as sell American Tower Corporation 130 towers for an upfront payment of $ 5 billion. Verizon is using $ 5 billion of this cash to repurchase shares. This comes to a 4% reduction at current prices.

In addition to its intelligent strategic moves, Verizon is seeing strong growth in its wireless segment. The company is benefiting as more-and-more consumers use increasing amounts of data on their smart phones and tablets. The trend toward more data has given Verizon a 7.5% earnings-per-share growth rate over the last several years.

Investors in Verizon should expect total returns of close to 12% a year from the company. Total returns will come from dividends (~4.4%) and earnings-per-share growth (~7.5%). Verizon appears fairly valued or slightly undervalued at this time with its price-to-earnings ratio of just under 15.

Final Thoughts

Warren Buffett (Trades, Portfolio) is possibly the greatest investor of all time. His portfolio is loaded with ultra-high quality businesses that are likely to compound shareholder wealth over long periods of time. With that said, being a prudent investor requires more than copying Warren Buffett (Trades, Portfolio)’s every move. Instead, intelligent investors should learn from Warren Buffett (Trades, Portfolio) and analyze his investments themselves to see if each matches your personal investing style. Examining the highest yielding stocks in Warren Buffett (Trades, Portfolio)’s portfolio is an excellent place to look for candidates to include in your dividend growth portfolio.