U.S. consumer confidence rebounds; existing home sales sink

U.S. consumer confidence rose to an eight-month high in December as inflation retreated and the labor market remained strong, but fears of a recession persisted, resulting in fewer households planning to make big-ticket purchases over the next six months. Other data on Wednesday showed sales of previously owned homes falling for a 10th straight month in November, the longest such stretch since 1999. The economy is on recession watch as the Federal Reserve, which is in the midst of its fastest interest rate-hiking cycle since the 1980s, wages war on inflation by trying to cool demand for everything from housing to labor.

“Consumers may be more confident than they were over the summer months, but they are still exhibiting more caution than was apparent in 2021,” said Sam Bullard, a senior economist at Wells Fargo in Charlotte, North Carolina. “The outlook for consumer confidence in 2023 will hinge on the Fed’s ability to deliver a soft landing on what could be described as a narrow runway.” The Conference Board said its consumer confidence index increased to 108.3 this month, the highest reading since April, from 101.4 in November. Economists polled by Reuters had forecast the index at 101.0. While the survey places more emphasis on the labor market, the rebound in confidence matched a similar rise in the University of Michigan’s sentiment index.Consumers’ 12-month inflation expectations fell to 6.7%, the lowest since September 2021, from 7.1% last month. The improvement, which mostly reflected lower gasoline prices, was in line with recent data showing consumer prices increasing moderately in November. It also strengthened views that inflation, though still uncomfortably high, peaked months ago.

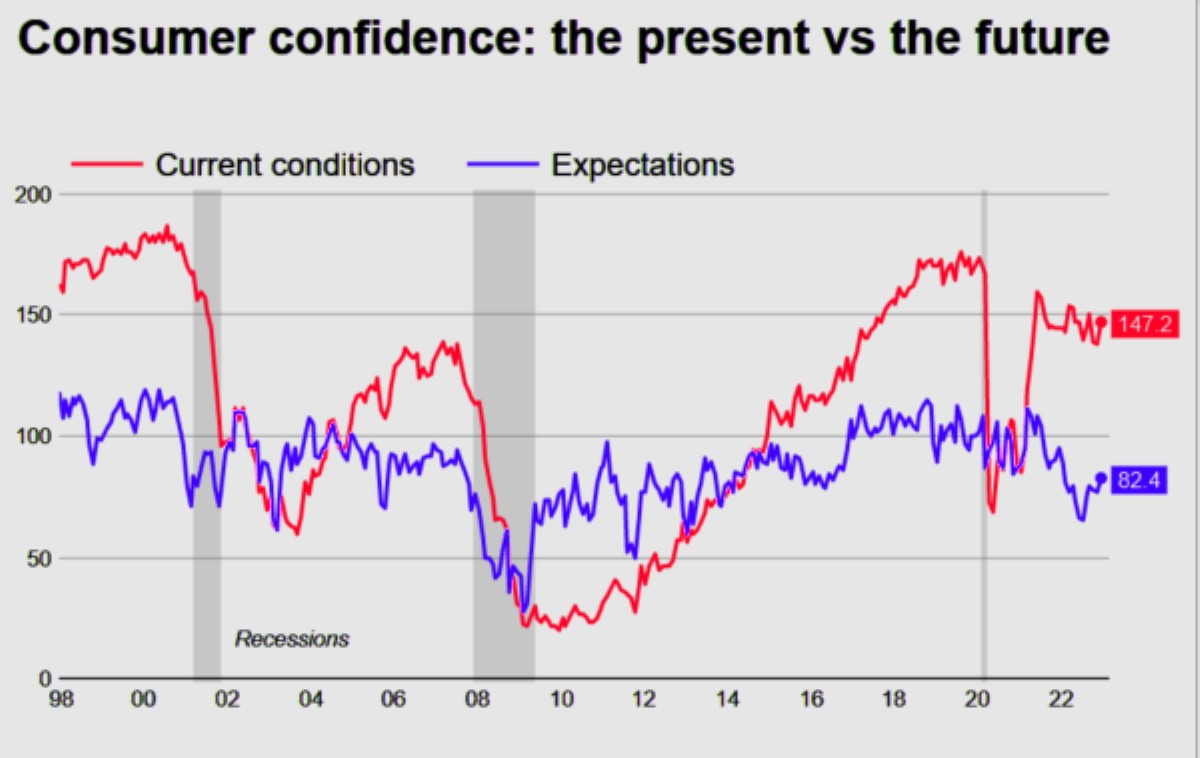

The present situation index, based on consumers’ assessment of current business and labor market conditions, rose to 147.2 from 138.3 last month. The expectations index, based on consumers’ short-term outlook for income, business, and labor market conditions, increased to 82.4 from 76.7. But this measure remains near 80, a level The Conference Board said was associated with recession. As a result, consumers were less keen on buying big-ticket items over the next six months. The share of consumers planning to purchase a motor vehicle was little changed, while intentions to buy appliances were the lowest since July.

That is also a function of higher borrowing costs as most of these goods are bought on credit. The Fed has hiked its policy rate by 425 basis points this year from near zero to a 4.25%-4.50% range, the highest since late 2007. Last week, the Fed projected at least an additional 75 basis points of increases in borrowing costs by the end of 2023. Consumers, however, planned to go on vacation over the next six months, with the share rising to 46.2% from 45.5% in November. Most intended to vacation locally, which could help to keep a floor under consumer spending.

The survey’s so-called labor market differential, derived from data on respondents’ views on whether jobs are plentiful or hard to get, increased to 35.8 from 31.5 in November. This measure correlates to the unemployment rate from the Labor Department and the rise in December was consistent with tight labor market conditions. Though there have been job losses in the technology sector and the interest over-sensitive housing market, employers have been generally reluctant to lay off workers after struggling to find labor during the COVID-19 pandemic.

But with the housing market in the doldrums, economists believe the labor market will loosen and unemployment increase next year. Though the housing market accounts for a fraction of the economy, it has a bigger footprint.Fewer consumers planned to buy a house over the next six months, which could keep homes sales on the back foot. Existing home sales tumbled 7.7% to a seasonally adjusted annual rate of 4.09 million units last month, the National Association of Realtors said in a separate report on Wednesday.

Outside the plunge during the first wave of the COVID-19 pandemic in the spring of 2020, this was the lowest level since November 2010. Sales dropped in all four regions and plummeted 35.4% on a year-on-year basis in November. Reports this week showed confidence among homebuilders dropping for a record 12th straight month in December, while single-family homebuilding and permits tumbled to a 2-1/2-year low in November. The housing market boomed early in the pandemic as Americans sought bigger properties to accommodate home offices, driving up prices beyond the reach of many.

Even with demand down, supply remains tight, keeping home prices elevated, though the pace of increases is slowing. The median existing house price increased 3.5% from a year earlier to $370,700 in November. It was still the highest house price for any November and prices remain about 37% above their pre-pandemic level. The average rate on a 30-year fixed-rate mortgage surged to above 7% a few months ago, the highest since 2002, according to data from mortgage finance agency Freddie Mac. Though the rate has since retreated to 6.31% last week, it is double what it was that time a year ago. “High rates make buying expensive for potential new homeowners, but they also tend to lock potential sellers in place given millions hold sub-4% and even sub-3% mortgages,” said Robert Frick, corporate economist at Navy Federal Credit Union in Vienna, Virginia. “We’ll need a thaw in mortgage rates before existing home sales warm up in 2023.”